Apologies if today’s post is not relevant to you. But if you’re approaching retirement or know someone who is close to retirement or know someone who has retired within the last 10 years, it might be worth reading on.

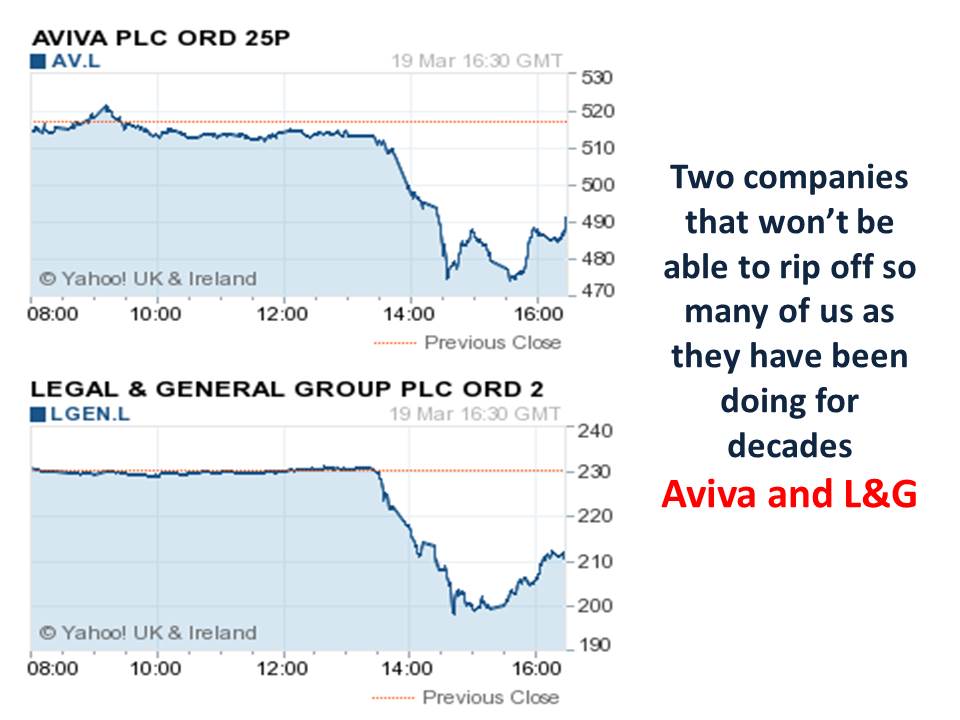

Yesterday’s budget was the usual tinkering dressed up to look like an economic policy – a penny off this, a few thousand more in tax-free savings and so on. But there was one truly revolutionary change – the�reduction in the pressure for people to buy an annuity in retirement. If you want to grasp how revolutionary this was, just look at�yesterday’s collapse in the share price of two companies that have been selling and mis-selling us rip-off annuities for decades – Aviva and L&G (click to see more clearly)

�

When you buy an annuity, you hand over your pension savings to an�annuity company in return for a guaranteed level of income for the rest of your (and, if you wish,�your partner’s) life. Annuity sales are falling as ever more people realise what a rip-off they are. But around 365,000 people a year are still buying annuities and at least�330,000 of them – 6,340 a week, 1,300 each working day – are getting ripped off by being sold the wrong annuity so they get many thousands of pounds less for their pension savings than they should.

If you know anyone approaching retirement, tell them to NOT, repeat NOT buy annuity. And if you know anyone who has retired and bought an annuity within the last 5-10 years, it’s probable they were mis-sold and should complain first to the annuity company and then to the financial ombudsman.

There are at least four things wrong with how annuities have been sold to us:

1. Excessive profits – The�pressure to buy an annuity, of course, meant that annuity companies could get away with selling us dreadful annuity policies,�which impoverished many pensioners, but made eye-wateringly excessive profits for the annuity companies

2. Not using OMO – A few years ago, after years of annuity mis-selling by the likes of Aviva and L&G, the financial regulator imposed a duty on pension companies to tell their customers that they didn’t have to buy their annuity from the company that held their pension savings. Instead they could use the Open Market Option (OMO) and buy from any annuity company to get the best rate for their particular circumstances. But while 85% of people would be better off using OMO, only around 40% do so. Thus 45% are getting fleeced�due to mis-selling or due to their own ignorance or passivity

3. Not getting an enhanced annuity – There is an impressively long list of medical conditions and if you have one or more of these when you buy your annuity, you’re entitled to an “enhanced annuity”. This means you get more money than a healthier person as your annuity company expects you to pop your clogs earlier. Around 65% of annuitants are thought to be eligible for an enhanced annuity, yet only 24% get one. Again�over 40% are being ripped off

4. Buying too early – About 6 months before you hit retirement age, your financial adviser or pension company will contact you to try to convince you to buy an annuity. Their sales pitch will be all about how an annuity will give you the security of an income for life:

Don’t believe it. All they want is to get your money as quickly as possible. In particular, they want to get your money before you qualify for an enhanced annuity – you may be fairly healthy at 65, but you can be sure you’ll develop some medical conditions by 70 or 75. If your financial adviser or pension company can get you to buy an annuity as early as possible, then if you do develop a medical condition or even die, tough! They’ve got your money – in fact it’s their money – and they have no need to pay you any more if you do get ill. Annuity contracts are irreversible.

In conclusion – Annuities are dreadful products. They give extremely poor value to customers while making massive commissions for salespeople and profits for annuity companies. They are often complex and usually mis-sold. And they should only be bought by a small minority of people, whereas currently around 90% of retirees are being conned into buying one.

There was no compulsion to buy an annuity anyway… I went into income drawdown 4 years ago and it was a good move, I took the TFC and maximum income each year with no loss of capital (so far) , Good to see the pension companies getting hit after years of shafting punters with rip off annuities

You’re right that the compulsion to buy an annuity has been weakened over time. But I understood that, until yesterday’s budget announcement, if a person didn’t have a retirement income of �20,000 (including state pension)they still had to buy an annuity by 75

I haven’t looked into it in any great detail but my wife yelled at me whilst she was watching the news and stated that we could all grab our pension pot as a lump sum. My first reaction was “bollox” That is also my second reaction too. We’ll have to wait and see when the budget is properly scrutinized.

The telegraph highlighted one aspect. HMRC can now raid your bank accounts if they perceive you’re pulling a fast one. The article seemed to have vanished (or maybe I missed it) as I wanted to read some of the comments, which were heating up nicely