I realise that on my blog, I probably sound too much like a Cassandra. But I genuinely try to bring stories that are not covered by the mainstream media. And remember, Cassandra was proved right.

Here’s�a story�that sent a chill through me:

The Government is planning to rename National Insurance (NI) by calling it��earnings tax�. The change, which will be proposed in legislation to be published in a few days, is the first step towards merging income tax with NI.

The Government claims, quite rightly, that this will�make the tax system more transparent.

Originally NI, which is charged on top of income tax, was first introduced in the National Insurance Act by Lloyd George in 1913 as a way for workers and employees to contribute towards certain benefits, such as a state pension. But now all the money taken for NI just goes into a general pot that the Government spends/wastes. The Government gets about �155bn from income tax and another �106bn from NI.

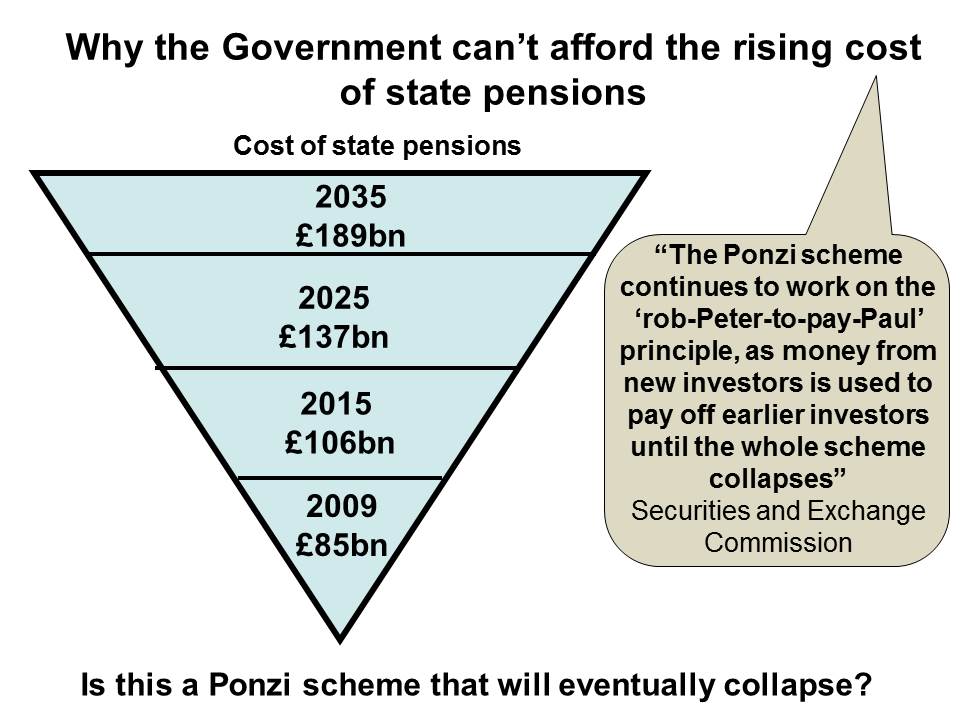

Now let’s just look briefly at the likely future cost of the state pension as the population ages (click on picture to see more clearly)

Whoops, it’s basically a Ponzi scheme – and all Ponzi schemes eventually collapse as there’s not enough money coming in to pay out.

So how can the Government avoid the state pension Ponzi scheme collapsing? By stopping paying a state pension to millions of people who have saved for private pensions.�And the way our Government will do this is by cutting any link between NI contributions and entitlement to a state pension. So the state pension will become just another “benefit” for immigrants, the poor and the feckless who have no savings or personal pension at all, rather than something people are entitled to due to having paid NI contributions for many years.

This name change signals a serious attack on the living standards of future pensioners, who may lose substantial amounts of money for the crime of providing a modest private pension for themselves.

The real victims of this coming massive con won’t be the rich. After all, losing the state pension of �100 or even �140 a week won’t make much difference to them. The real victims will be the millions who have been coerced into paying into the new�Workplace Pensions that have been so eagerly advertised by a few well-known multimillionaire businesspeople (Theo, Karren, Nick and others�in the “We’re in” TV ads). If the Government does turn the state pension from an entitlement into a benefit, all these savers will find is that their savings into the new Workplace Pensions�scheme will disqualify them from receiving a state pension.

Many years ago, I opted out of the SERPS scheme and put my money into a private pension because I didn’t trust any government. Just as well, as this Government�is abolishing SERPS and (if I understand the situation correctly)�anyone�who had paid�in will have wasted their money. Now I could, if I want, pay NI for my wife. But I’m not going to as I believe that by the time she reaches pension age, her savings will mean she gets no state pension and all money I would have paid in NI will be wasted. Instead I’ll provide�a private pension for her because I�still don’t�trust this or any other government.

I was at the UKIP conference last summer, and their guest speaker was the Labour peer, Lord Digby Jones.

http://www.youtube.com/watch?v=FZ3nWrtYTwo

He might have worked for the last Labour government, and his personal beliefs and former voting pattern do not come into it, as he was/is a businessman first.

The main thrust of his speech was that from the day that the National Insurance scheme was announced, we have not been able to afford it… As you say David, it is a Ponzi scheme, and the perpetrators/managers of that scheme, i.e. the governments that have “governed” since then have known this, but they have never had the honesty or the guts to tell the people who have been forced into it.

As you say, ultimately the only beneficiaries will be people that have never paid a cent into the scheme… So called benefits claimants.

Some time ago I read an article regarding the above item. After weighing up all the different options the author settled on the ISA as the best investment for your pension. So much so, that as long as all ISA’s were left invested, one could become a millionair. However, there is a caveat; due to the BOE, ie the goverment, and its almost zero interest rate policy, this form of investment is not as lucrative as it once was. That said, it is still the best way to secure your future retirement. At least there are no fees to pay, and make someone else rich at your expense.

[…] written before about why I think the state pension will eventually be abolished http://www.snouts-in-the-trough.com/archives/8608�Last night I found out how this will […]

A brilliant article explaining how the usual suspects are planning to remove our trousers and stuff us up the a***.

Incidentally, your book “GREED” is an excellent read and should be compulsory reading for all school leavers to assist them in making their decision to emigrate to Australia before wasting their lives working to prop up the establishment of londonstan and its U.K. colonies.

You need to get this book better advertised as I am sure it would appeal to a much wider audience if only people new it existed.

keep up the good work !!

The casual leaking of the new that Osborne thought about ‘merging’ N.I. and Income tax sent a chill through me this morning.

I agree with your thinking about any future Governments needs to cap/scrap automatic pensions to those that have paid their N.I. contributions…but was shocked to see that the wheels are in motion so soon!

Aw, this was an incredibly nice post. Taking a few minutes and actual effort to generate

a top notch article… but what can I say… I procrastinate

a whyole lot and don’t manage to get anything done.